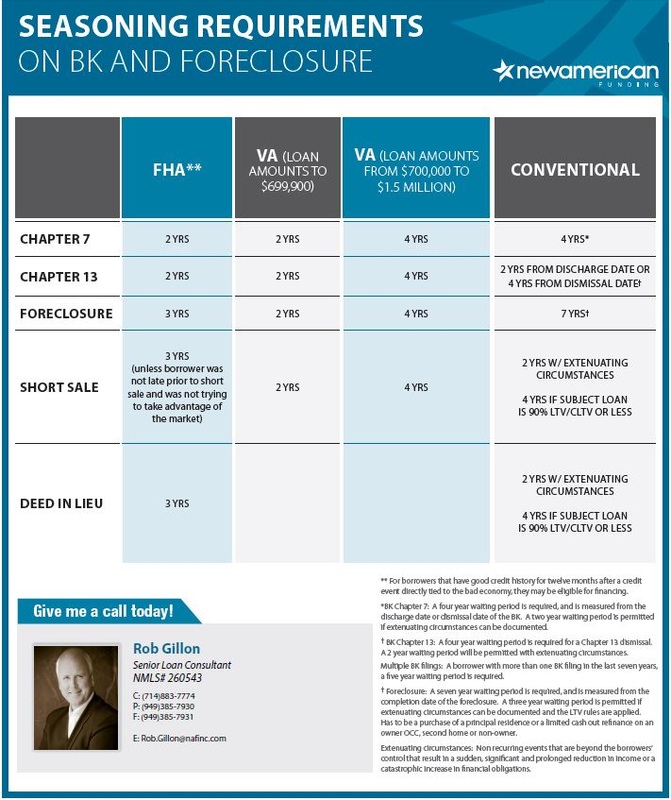

A common question a lot of homeowners ask me is how quickly will they be able to get back into the housing market.

Mortgage lending guidelines constantly change, and banks have tried to regulate the qualifying process in hopes of avoiding a repeat of the 2006 mortgage meltdown. Call or email me with any questions you may have!

0 Comments

Talking to your bank can be stressful. The constant phone calls can feel like harassment, and a lot of people ignore their banks completely.

However, the banks sometimes have important information regarding your options to foreclosure, and the only way to get their help is to take the phone calls. Here are a few tips to get the most out of your conversations with your bank representative:

While moving can be stressful, being prepared and organized can make moving a lot easier. Here are a few guidelines to help make the process as smooth and stress free as possible:

6-8 Weeks Prior:

4-5 Weeks Prior:

2-3 Weeks Prior:

1 Week Prior:

Moving Day

The million dollar question. The most common question I'm asked regarding a short sale is "how long will this take?" Unfortunately, that's difficult and almost impossible to accurately pinpoint . There are so many factors that affect the short sale process, and here are a few that will determine how long it will take from start to close.

While sellers' preferred time frames vary considerably, banks are trying their best to get their short sales processed and closed. Stalling for too long, or having an unresponsive bank can put you in danger of foreclosing, and the ramifications of foreclosure are often considerably more negative than those of a short sale. In general, I'm seeing the approval process take about 60-90 days. This is the time form when we submit the complete short sale package (your financial paperwork & an offer) to receiving the approval letter from your bank. Once we have the approval letter from your bank, we open escrow. Escrow generally takes an additional 30 days. If you are considering a short sale, NOW is the time to act. As of right now, the deadline to apply for a HAFA short sale (with it's $10,000 closing incentive) is 12/31/2016, so CALL US TODAY!

If you have some equity in your home and you're thinking of selling, getting top dollar is usually the first focus. Sellers with the ability to update and renovate can command higher resale prices. While renovating may not be in everyone's budget, there are things that can be done that cost little or no money. Here's a short list of items that you can do if cash is tight:

There are other fixes you can do if you have a few dollars to spend. Get creative but try to keep color palette neutral and (yes) on the bland side.

Grey is the "in" color at the moment, and if you've visited as many new model homes as I have in the past year or so, you'll see that all the builders are decorating with grey hues and tones. Soothing, calm and sophisticated is the way to go! While a complete remodel may not be financially feasible, remember, small inexpensive (or even free!) changes can reap big dollar returns!  One of the challenges facing sellers with compromised credit is finding a new home to move in to. Difficulty in making mortgage payments often leave homeowners with less than perfect credit. While landlords obviously prefer good credit, finding a rental is not always as difficult as you may think.

One of the things I tell my clients when they're considering transitioning into a rental property is to try and keep their other monthly payments current. Landlords are aware of the difficult economic climate, and are often sympathetic to missed mortgage payments if other monthly payments are kept current. These payments include credit cards, car payments, cell phone bills, utility bills, student loans, and all other revolving debt. If your other payment history is less than perfect as well, a letter of explanation will often go a long way. Did you have medical issues, job loss, increased expenses, etc.? A heartfelt, truthful explanation will often help sway things in your favor. Also, complete honesty and transparency in your application is KEY. Everything pops up on your credit report, so any discrepancies between the two (and landlords almost ALWAYS require a credit report) will raise HUGE red flags. I have also had clients agree to payroll direct deposit as a way of assuring the landlord that rent will be paid in a timely manner. If your employer has direct deposit, you can agree to arrange to have your rent paid directly to the landlord's account from your employer. Landlords often ask for bank statements with the application to rent. If you can show money in a savings account, this will help your chances of securing a rental as well. Call me with any questions regarding finding a rental, I'll be happy to assist in any way I can! |

RSS Feed

RSS Feed